Common Myths Related To Hurricanes & Homeowners Insurance

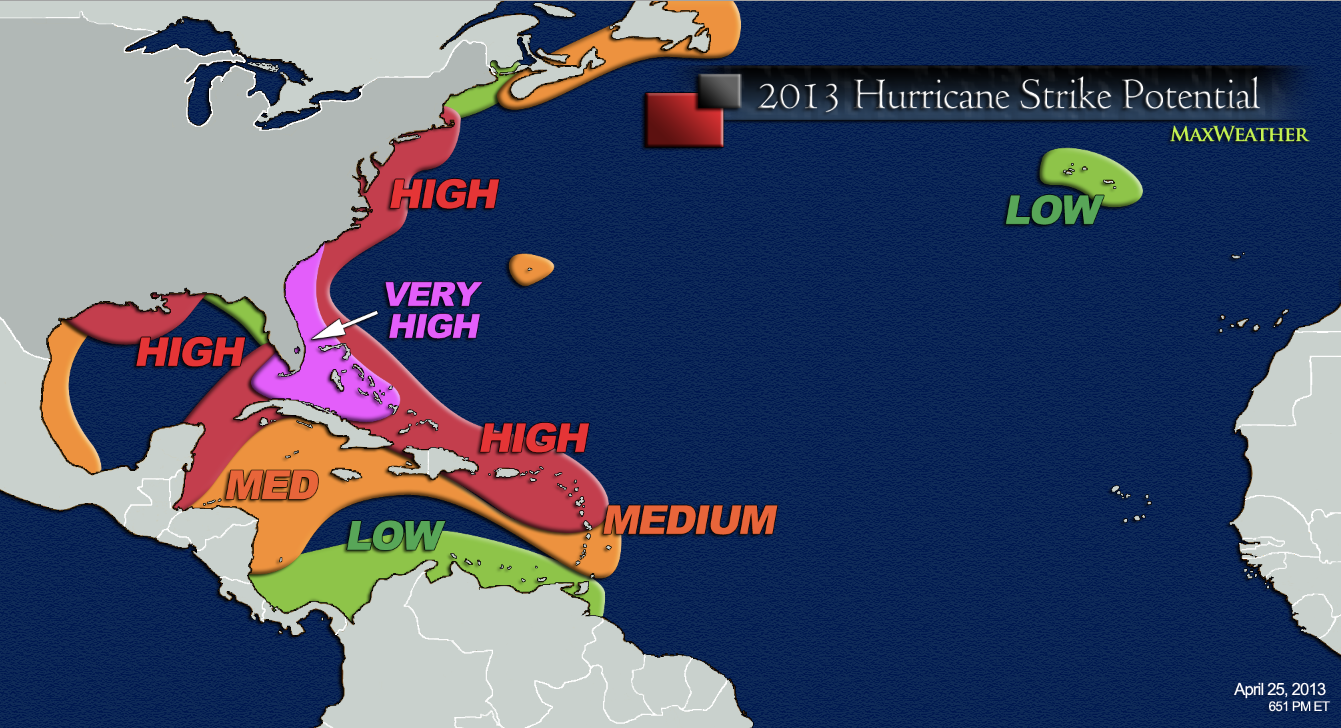

2013 Hurricane Season Strike Potential

While the first part of hurricane season has been relatively quiet this year you never know when a big one will hit and it pays to be prepared. Last years Superstorm Sandy didn’t hit until late October but when it did it packed quite a punch. Sandy flooded over 150,000 homes and killed 140 people. A total of 8.5 million homes scattered over 20 states were left without power.

It doesn’t take a storm like Sandy to damage your home, even a minor one can cause significant damage when high winds are combined with torrential rain. If you have the unfortunate luck of having your home damaged in a storm you will probably have lots of questions about your homeowners insurance coverage.

A Consumers Report survey found that out of 8,000 people who survived SuperStorm Sandy only 54 percent of those who filed claims were highly satisfied with the way their claim was handled. Having a clear handle on what is actually covered by your policy will make your claim go smoothly and ensure that you are completely covered this hurricane season.

Common Myths Related To Hurricanes & Homeowners Insurance

Here are a few common myths related to hurricanes and homeowners insurance:

Disaster coverage is offered by most standard homeowner policies.

The reality is that most standard policies do not offer coverage for floods, hurricanes, and earthquakes. Protection for these disasters is usually available at an additional cost, but in some areas flood insurance may be hard to come by. According to the Consumers Report survey 30 percent of respondents did not have flood insurance.

Check with your agent or insurer in regards to exclusions on your policy. If you live in a disaster prone area consider buying any additional coverage you need. Prepare for hefty premiums when it comes to disaster insurance.

My insurance payout will be the current market value of my home.

According to insurance experts, many homeowners are underinsured. It is the homeowner’s responsibility to update their insurance policy to the true value of their home. If you have made upgrades to your home which have increased its value be sure to update your homeowners insurance. The same is true if home values in your area have been climbing.

Review your policy on a regular basis and ask your agent for an estimate of the replacement cost of your home. If necessary, up your coverage levels.

Your claim will be handled quickly.

While you may be lucky and your claim will be settled quickly there is a good chance you will end up in a fight with your insurer, especially if it is a big claim. You will need to provide lots of documentation in regards to your personal property. You will often be required to provide purchase dates and even serial numbers for more expensive items.

It is highly recommended that you do a home inventory and keep it updated. There are plenty of apps available that make this tedious task a bit easier. Be sure you keep a copy of the file in the cloud or in a safety deposit box. If you are disputing your insurers offer, get your own contractor to produce an estimate.

If a neighbor’s tree falls on my car or house, his/her insurer will need to pay.

Unfortunately, this is not true. Unless the tree was a neglected hazard, meaning it was completely rotted prior to it falling you will need file a claim with your insurer for the damage.

If you spot any obviously dead trees in your neighbors yard bring them to the attention of your neighbor. Sending an email will provide documentation if you end up in a fight over the claim later. Take photos as well. If they refuse to deal with the hazard, notify the proper authority in your town or city.

The hurricane season is in full swing so make sure that you fully understand your insurance policy and make sure you are completely covered against disaster damage.